Profit & Loss Statement with Sleek Bill Your Guide to Financial Clarity

Profit and loss statement is giving an overview of total business income versus total expenditure. It helps to calculate profit of business. Sometimes we profit loss statement called as income statement or statement of earnings. It helps to check and analysis of business over financial month. It is very easy and efficient with Sleek Bill to create accurate and professional Profit & Loss Statements for such decision-making and legality compliance requirements.

Learn the term Profit & Loss Statement, and its importance?

A Profit & Loss statement is an detailed accounting document that calculates the revenues, expenditures, and profit or loss made in a certain accounting period, generally one year. It is financial statement that involves detail information of total revenue and expense of businesses. It helps businesses understand:

The Financial State of the Organization: It gives a concise description of the financial performance.

Help in Decision Making: Prepare budgets and control costs while making investments.

Legal Compliance: Required for tax purposes and compliance with regulations.

Key Components of a Profit & Loss Statement

A well-maintained Profit Loss statement includes essential details such as:

Sales: Total amount of product sold to customer. product amount to be sold to Clients or dealers.

Purchase : Total amount of product is purchased from vendor.

Credit Note: The total amount which credited from vendor or supplier or money back to returned goods or service to vendor.

Debit Note: The total amount which payback to customers retuning sold product from customer or buyer.

GST: Total tax required to pay this is amount count in expenses.

TDS: Tax Deducted at Source 2% rate on payments made to the supplier or vendor of taxable product or service. This amount is count in expenses.

TCS: Tax Collected at Source. This every e-commerce needs to collect 0.5 %.

How to Prepare a Profit & Loss Statement

There are two main accounting methods for creating a P&L statement:

Cash Basis of Accounting

Records transactions when cash is received or paid.

Simple but less accurate; suitable for small businesses.

Does not support audited financial statements.

Accrual Basis of Accounting

Recognizes revenue and expenses when earned or incurred, regardless of payment timing.

Provides greater accuracy and is required for audited statements.

Ideal for businesses of all sizes seeking detailed insights.

How a Profit & Loss Statement Differs for Service-Based and Product-Based Businesses

Service-Based Businesses

Primary revenue comes from fees or rents.

Expenses are recorded as "cost of revenues.

Profits may include income from selling intellectual property.

Product-Based Businesses

Revenue is generated from sales of goods.

Uses the term "cost of goods sold" (COGS) to reflect production costs

Profits are derived from selling physical inventory.

Why is a Profit & Loss Statement Essential for Financial Planning?

A Profit & Loss Statement:

Tracks Performance: Helps businesses monitor profitability and operational efficiency. The profit loss can gives loss or gain of business.

Supports Growth Forecasting: Each and every business can generate revenue which turns into profit. This tells how much money your brought to doing sales of goods or services. Projects future performance based on historical data.

Guides Resource Allocation: Identifies areas to cut costs or invest more. Cost required to day to day business includes in expenses. Expense includes rent, taxes, purchased cost of materials or product from vendor, wages of employees of business.

Enhances Tax Compliance: Provides accurate data for tax filings and audits.

How to Generate a Profit & Loss Statement in Sleek Bill

Sleek Bill makes maintaining an Inventory Book simple and efficient. Follow these steps to get started:

Log In: Visit sleekbill.in and log in with your credentials. New users can sign up for an account.

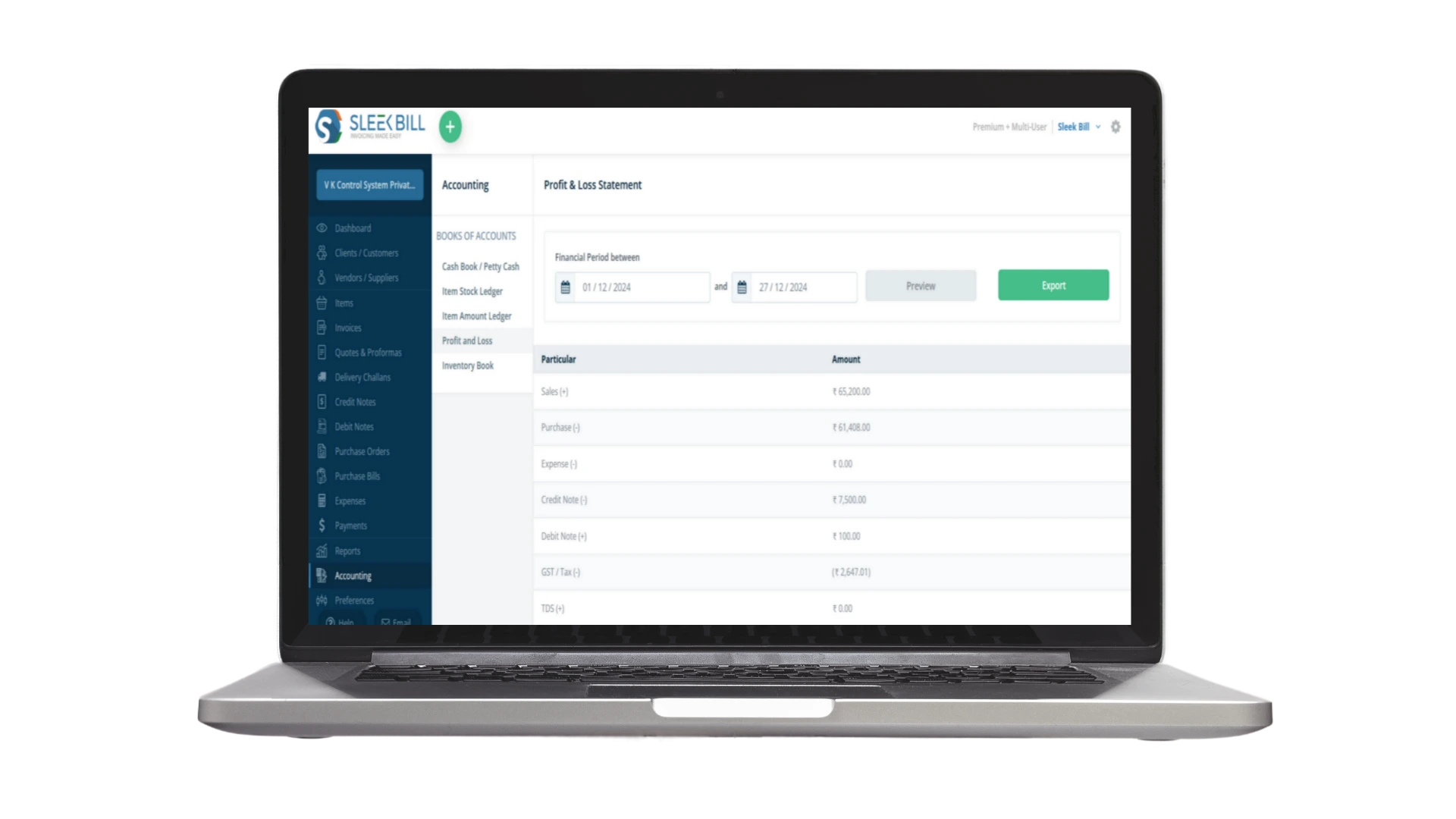

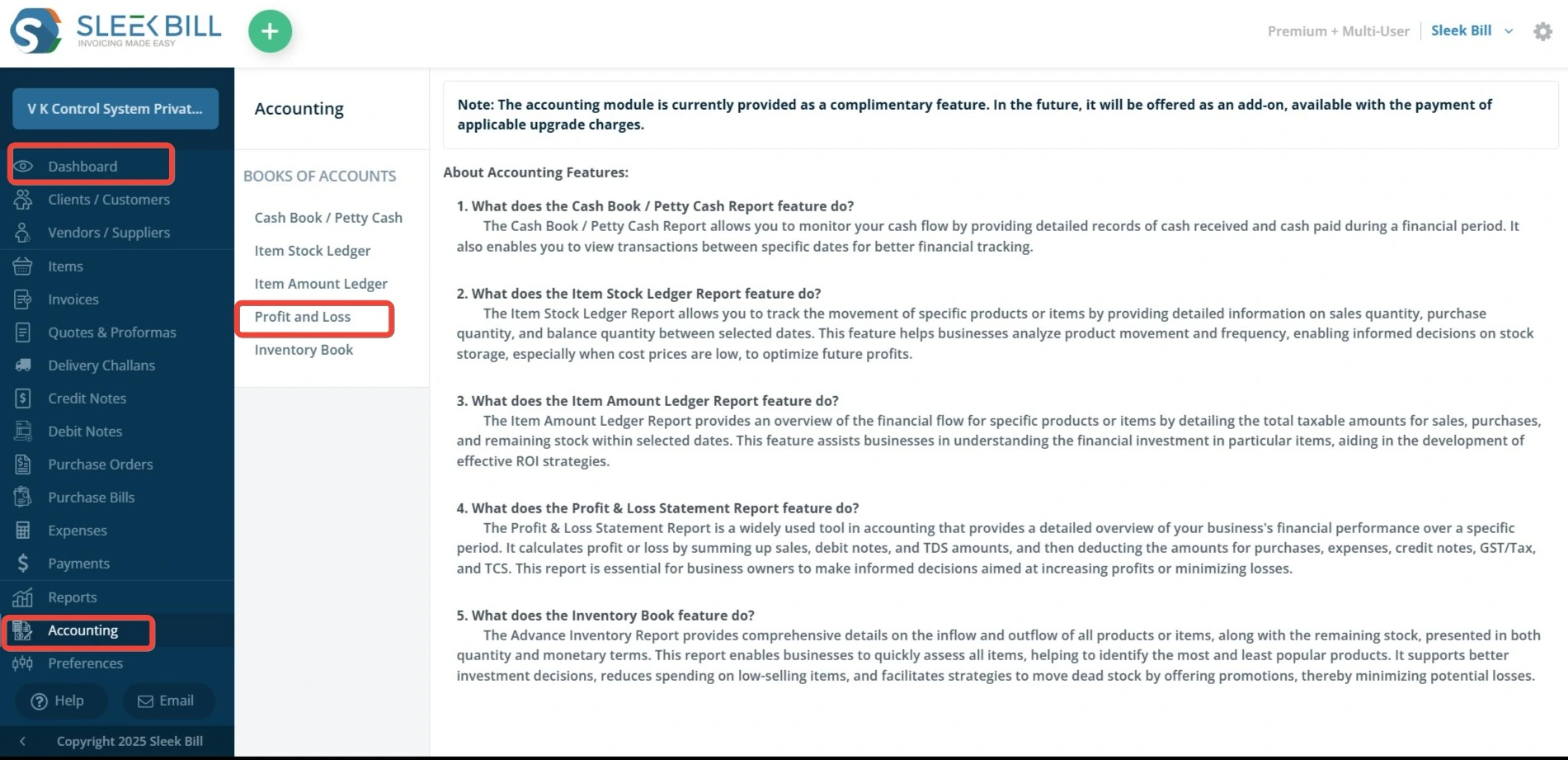

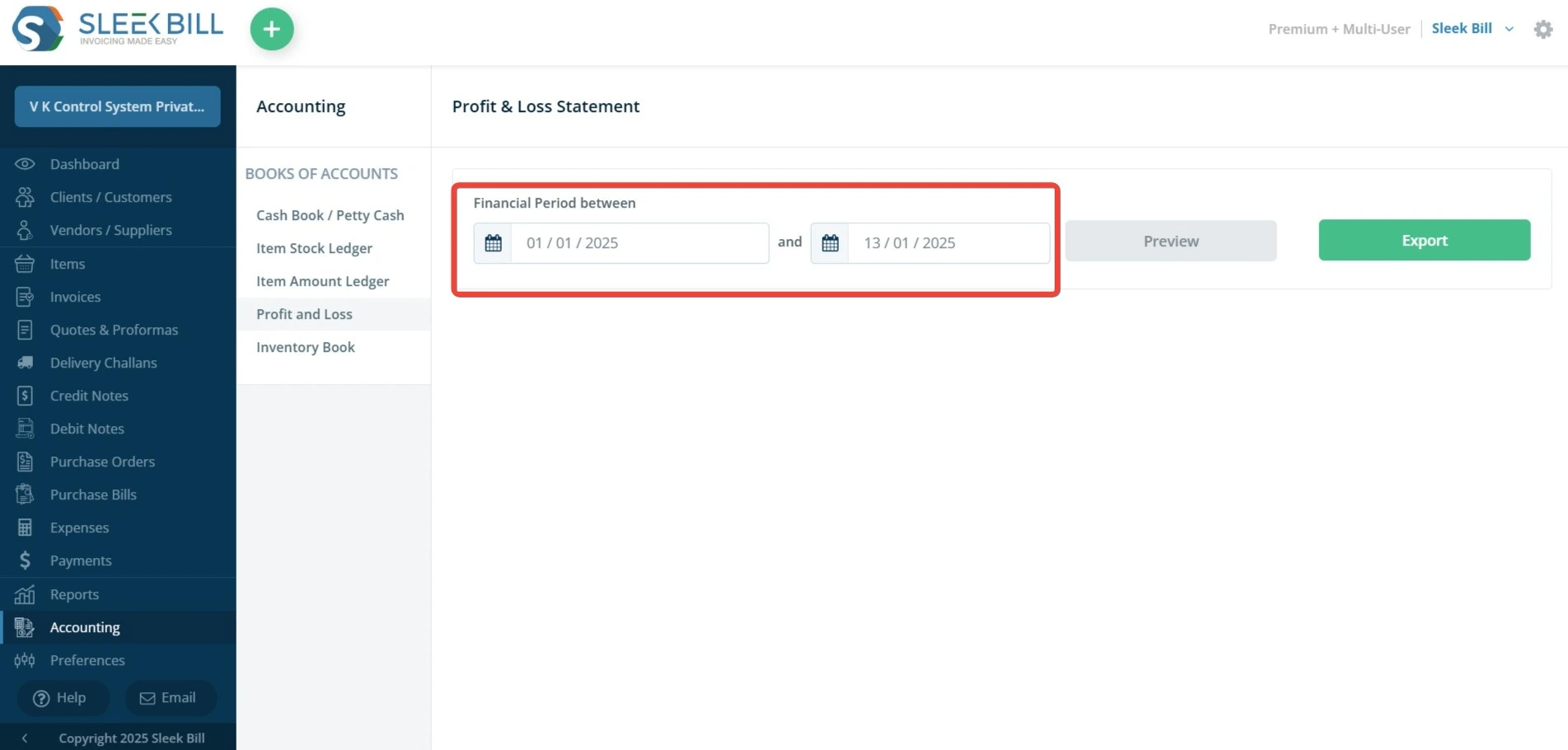

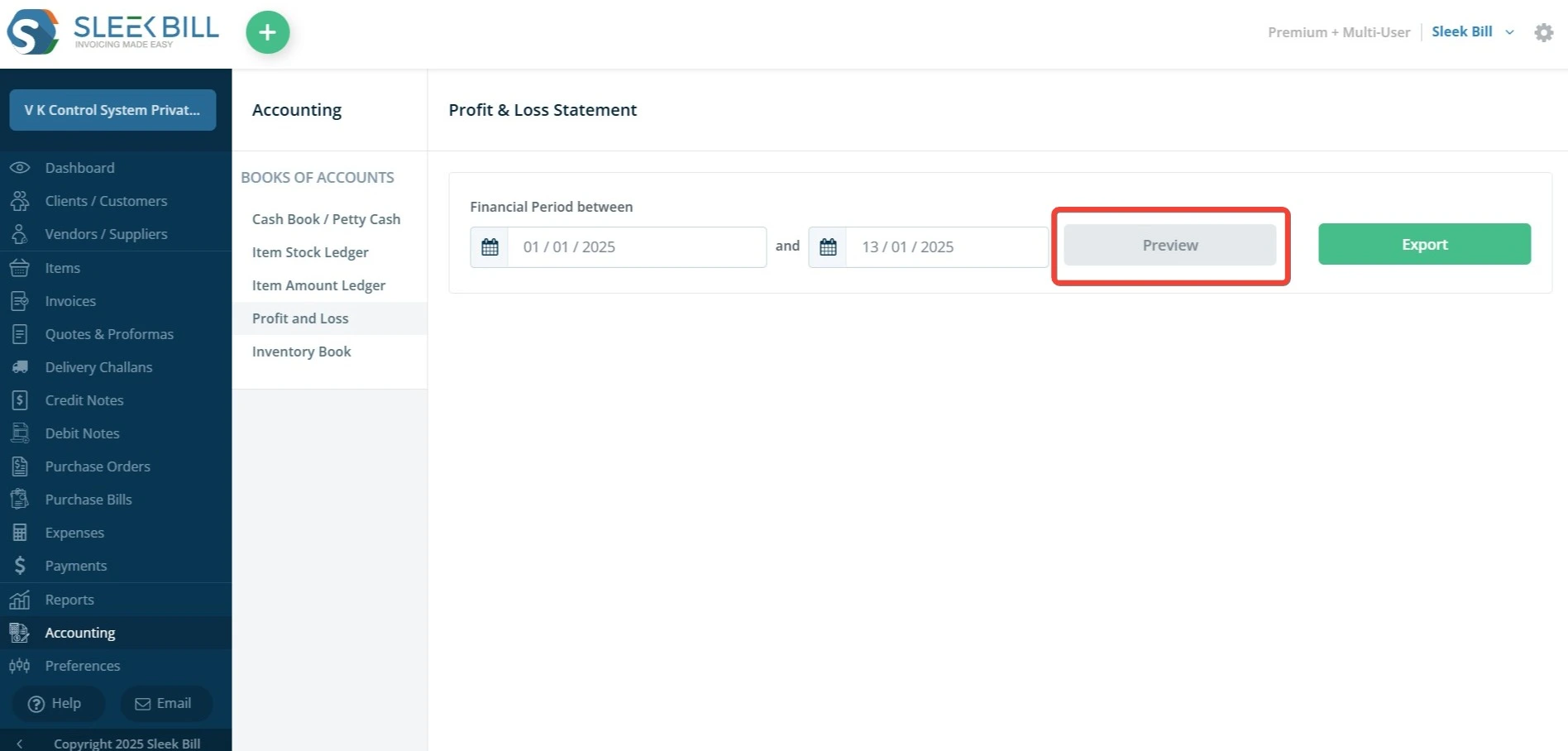

Access Inventory Book: Go to Accounting > Profit & Loss.

Select Financial Period:

Choose the date range for which you want to generate the statement.

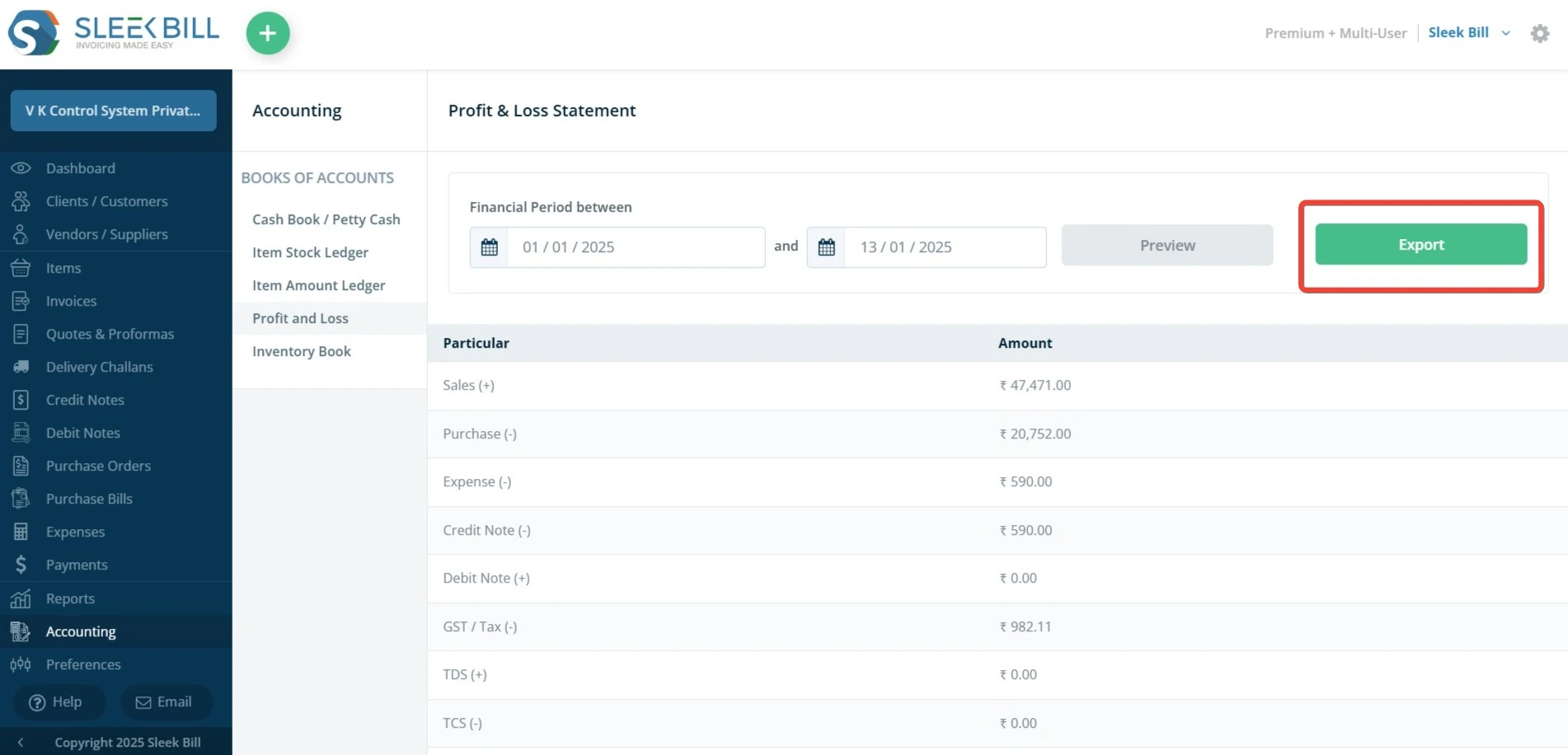

Preview the Statement: View the statement to check sales, purchases, expenses, taxes, and total profit or loss.

Export the Statement: Download the P&L statement in Excel format for record-keeping or further analysis.

Common Mistakes to Avoid When Preparing P&L Statements

Data Entry Errors: Double-check all inputs to ensure accuracy.

Neglecting Accounts Receivable: Include all outstanding payments.

Misclassifying Expenses: Ensure proper categorization for accurate analysis. Putting costs in wrong categories. For example confusing operating expeses like rent or payrolls, purchase cost.

Failing to Reconcile Accounts: Regularly verify balances to avoid discrepancies. Business is profitable on paper but shortage of cash. It happen unexpected financial burdens.

Lack of Backups: Always save and back up financial data.

How a P&L Statement Connects with Other Financial Statements

The Profit & Loss Statement works closely with:

Balance Sheet

The document which exhibits the various positions of the company at a particular time.

Cash Flow Statement

Tallies the actual cash inflows and cash outflows for the period specified. These together present a complete picture of a business's financial condition.

Tips for Small Businesses

Use Tools Like Sleek Bill:

Automate calculations and report generation.

Save time and reduce errors.

Analyze Trends:

Compare P&L statements over different periods to spot patterns.

Focus on Key Metrics:

Gross margin, net profit, and expense ratios.

Customize Reports:

Tailor P&L statements to meet specific business needs.

Profit & Loss Statement Template for Startups

Startups can use a simple P&L template that includes:

Business name and report period.

Expense categories (e.g., marketing, salaries).

Revenue categories (e.g., product sales, service income).

Net profit or loss at the bottom.

Automation and Software Integration

Manual P&L statement preparation can be time-consuming and error-prone. Sleek Bill offers:

Profit & Loss Statement is a good projecting element to know by understanding it very well and then ameliorating your business in terms of its financial health. By modernizing this tedious and most important ritual at an automated yet specific way of Sleek Bill, no business should worry about its accuracy, compliance, or timelines of data insights. Whether you're a small proprietor or managing a trunk of giant enterprise, Sleek Bill helps you to concentrate on growing your business by letting a reliable tool take care of the report on financing.

A Profit & Loss Statement (P&L) is a financial report that summarizes a business’s revenues, costs, and expenses over a specific period. It helps evaluate the company's financial performance and profitability.

It provides insights into the profitability of your business, helps in tracking expenses, and is essential for decision-making, securing loans, and meeting tax requirements.

Sleek Bill simplifies the process by automating calculations and providing an easy-to-use platform to record income and expenses, ensuring accurate financial statements.

A Profit & Loss Statement focuses on income and expenses over time to show profitability, while a Balance Sheet provides a snapshot of your business’s assets, liabilities, and equity at a given point.

It’s common to prepare P&L statements monthly, quarterly, or annually, depending on your business needs and reporting requirements.

GST Invoice Format

GST Invoice Format

GST Billing Benefits

GST Billing Benefits

GST Credit Note

GST Credit Note

GST Online Advantages

GST Online Advantages

Free training & support

Free training & support 60K Happy Customers Worldwide

60K Happy Customers Worldwide Serious about

Serious about